Airbnb Recovery & COVID-19: Data Insights

This is The TechCrunch Exchange, a newsletter distributed on Saturdays, stemming from the column of the same name. You can subscribe to receive the email here.

DoorDash submitted its IPO paperwork on Friday, indicating that we will see at least one more unicorn public offering before the year 2020 concludes. I previously analyzed the key figures, Danny reported on the parties who stand to benefit from the offering, and I considered the effects of COVID-19 on the company’s performance.

This leads me to another COVID-19 affected unicorn that is anticipated to become a public company in the near future: Airbnb.

When Airbnb initially filed for its IPO in August, the outlook appeared promising. The company was generally believed to be recovering from the difficulties caused by COVID-19, the public markets were receptive to growth and technology stocks, and the number of COVID-19 cases in the United States was decreasing from its summer peak. It seemed ideal for Airbnb to finalize its Q3 results, release its public S-1 filing with the updated figures, and capitalize on investor confidence, demonstrating that even a worldwide pandemic and a downturn in the travel sector couldn’t hinder its progress.

However, the United States and the global community are currently experiencing the most significant surge in COVID-19 cases to date, and consumer spending is decreasing just before the release of the company’s S-1 filing. November presents a less favorable environment for an Airbnb recovery than August or September did. Nevertheless, when Airbnb files – reportedly next week, so please be prepared – we will only have access to its financial data through the third quarter.

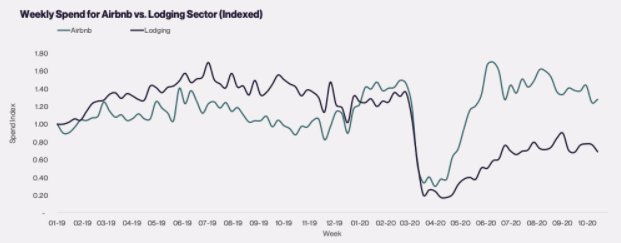

This timeframe aligns with a dataset provided by Cardify, which I have examined. According to the company, which monitors consumer spending in real-time, here’s a comparison of Airbnb’s recovery relative to the broader industry following the initial decline in lodging expenditure during the pandemic:

A noteworthy result, isn’t it? Unfortunately for Airbnb, the initial surge in demand from late June through July gradually subsided over time.

Examining the data more closely, here’s a comparison of Airbnb spending from July 2020 through the end of October, the first month of Q4, with the same period in 2019:

Although declines are evident, the data remains encouraging for the company. I wouldn’t have anticipated Airbnb spending – based on third-party data – to be this robust.

The trend of individuals renting homes for a month appears to have lessened, should you be considering this when evaluating Airbnb’s revenues from the charts above. Cardify informed TechCrunch that after reaching approximately +70% in March-April, “average booking sizes have now stabilized and are roughly 30% higher on a year-to-date basis.”

The charts indicate a weakening trend in October, but this seems at least partially attributable to seasonal factors, given the 2019 data. Therefore, I hesitate to attribute the decline solely to increasing COVID-19 cases. However, this downward trend was also observed in comparable data from SimilarWeb, which was also shared with The Exchange. Their dataset, tracking accommodation booking volume globally for various travel services, including Airbnb, revealed that a bookings recovery through September, which had partially offset March lows, was reversed by October declines. Europe’s bookings recovery peaked in July and has been decreasing since then. Asian volume is increasing, but remains significantly lower than previous levels.

The overall picture is mixed, but given that Airbnb is performing better than the broader industry according to Cardify, the aggregated data may be leading to a more pessimistic assessment than necessary. We will soon have access to the actual figures, but I wanted to share my observations with you. Now, onto the S-1 filing!

Prior to DoorDash’s filing, we had planned to discuss Brex in this section today, following Airbnb. However, due to increased activity, expect those insights early next week on The Exchange.

Market Notes

This past week featured a heavy schedule of earnings reports, so I’ve compiled some observations from discussions with various companies following their announcements. Please excuse any omissions regarding preferred reporting sources, as space is limited.

Appian significantly exceeded earnings expectations. The driving force behind the growth of this low-code application development services provider? According to CEO Matt Calkins, it wasn’t attributable to a single factor. Rather, the company’s success stemmed from a sustained period of progress, although he also noted that awareness of low-code solutions has recently increased substantially among the general public.

What accounts for this shift? The disruptions experienced this year accelerated the adoption of new business practices at a rate faster than anticipated. This outcome underscores the reality of accelerating digital transformation, which is a positive indicator for emerging companies. (Further information on Appian and the low-code sector can be found here.)

Alteryx provided The Exchange with a unique opportunity, featuring both outgoing CEO Dean Stoecker and incoming CEO Mark Anderson to discuss their results. The company surpassed expectations for the third quarter, but its projections for the fourth quarter failed to generate enthusiasm among investors. What explained this discrepancy? Anderson posited that Annual Recurring Revenue (ARR) growth offers a more transparent and accurate representation of an expanding software company than traditional GAAP revenue forecasts. While acknowledging the importance of revenue, he emphasized the need to focus on ARR due to the complexities inherent in revenue recognition.

Alteryx has established a strong ARR target for 2021. It remains to be seen how investors will react to the fourth-quarter results and whether they will adopt the perspective of the new CEO. The former CEO expressed confidence, stating that the market will eventually recognize the central role of analytics in digital transformation, and that his company will be well-positioned to capitalize on this trend.

Shifting gears, earlier this week I inquired with several venture capitalists about the software venture capital landscape following Monday’s significant market downturn. I asked about the potential impact on both public and private software companies if other investment options became more appealing—initial optimism sparked by positive vaccine news on Monday was later tempered by a resurgence of cases throughout the week, and Zoom experienced a substantial loss in value as investors sold off shares.

Responses arrived later than expected, but I wanted to share them nonetheless, as they were more optimistic than I had anticipated. Laela Sturdy, a general partner at Alphabet’s Capital G, believes that “private software investors are unlikely to substantially alter their investment strategies in response to public market fluctuations,” and later added that “public market changes would need to be exceptionally severe—a decline of 30 percent or more—to significantly affect growth-stage valuations.”

A connection exists between public valuations, trading activity, and private capital allocation, but the strength of this link varies depending on current circumstances. Currently, it appears that private investor enthusiasm for software remains robust.

Sturdy elaborated on the reasons for this resilience: “Underlying long-term trends, including the increasing adoption of cloud technologies, automation and artificial intelligence, data analytics, cybersecurity, financial technology infrastructure, and the continued rapid pace of digital transformation, will enable tech companies to remain attractive to growth investors in both the private and public sectors.”

- Hopin secured $125 million in funding at a $2.125 billion valuation after achieving $20 million in ARR in less than a year. Impressive!

- Earnings reports from Square and PayPal suggest a favorable outlook for fintech startups in general, although investment appears to be concentrated in the more mature segments of this sector. (TrueBill recently raised $17 million, for example.)

- Udemy is seeking an additional $100 million in funding.

- What does the future hold for edtech startups given the recent decline in edtech stock prices?

- Menlo Security obtained $100 million in funding at an $800 million valuation. A strong result!

Various and Sundry

Lastly, here’s a collection of items I didn’t have time to cover earlier this week. Let's dive in:

- I had a discussion with Cambridge Innovation Capital, an interesting venture capital company based in Cambridge, United Kingdom – distinct from the Cambridge located on the U.S. East Coast. Further details will follow, but it’s encouraging to see innovation centers globally evolving into robust startup ecosystems.

- I received an advance copy of a Limited Partner (LP) survey conducted by Allocate. Scheduled for release on Monday, the survey indicated that “just 20% of [LP] respondents reported that COVID-19 had hindered their investment pace,” providing context for the significant fundraising activity observed in recent months.

To conclude with an enjoyable note, recall our analysis of startup performance during the third quarter? That was quite insightful. In related news, JotForm, a no-code “online form builder,” shared with The Exchange that its revenue has increased by 50% compared to its 2019 figures, its enterprise client base has grown by 620%, and it anticipates achieving “100,000 total paying users by year-end.” That’s impressive!

Alex