SPACs Explained: The Circle Example

Circle to Go Public via SPAC: A Deep Dive

Following Coinbase’s public debut earlier in the year, several other cryptocurrency firms are now considering accelerated paths to becoming publicly traded. Circle, a Boston-based financial technology company specializing in API-driven financial services and the issuance of a stablecoin, appears to be among them.

A Different Route to the Public Market

Unlike a direct listing or traditional IPO, Circle is opting to merge with Concord Acquisition Corp., a special-purpose acquisition company (SPAC), often referred to as a blank-check company. This transaction establishes an enterprise value for Circle at $4.5 billion, with an equity value of approximately $5.4 billion.

This move represents a noteworthy development within the cryptocurrency landscape. Where Coinbase’s business model – a trading platform generating readily understood fees – is familiar to conventional investors, Circle’s services are comparatively more nuanced.

Understanding Circle’s Business

Circle’s investor presentation highlights a business centered around a stablecoin, a cryptocurrency designed to maintain a stable value relative to a fiat currency, specifically the U.S. dollar. The company also provides a suite of APIs that enable other businesses to integrate cryptocurrency-based financial services.

Furthermore, Circle owns SeedInvest, a platform for equity crowdfunding. However, the majority of Circle’s projected revenue is expected to originate from its core stablecoin and API offerings.

Analyzing the Deal and Future Prospects

TechCrunch’s Romain Dillet has provided detailed coverage of the transaction itself. Our focus will be on dissecting Circle’s investor presentation, examining its business model, and analyzing its historical performance, projected results, and resulting valuation multiples.

Essentially, this provides an opportunity for a thorough financial assessment. Let's proceed with the analysis.

Key Components of Circle’s Strategy

- Stablecoin Issuance: Circle’s primary function involves the creation and management of a stablecoin pegged to the U.S. dollar.

- API-Driven Financial Services: The company offers a range of APIs allowing businesses to incorporate cryptocurrency functionality into their own platforms.

- Equity Crowdfunding (SeedInvest): Circle’s ownership of SeedInvest expands its reach into alternative investment opportunities.

The combination of these elements positions Circle as a key player in the evolving cryptocurrency ecosystem. The SPAC merger will provide the capital needed to further develop these services and expand its market presence.

Understanding Circle’s Operational Framework

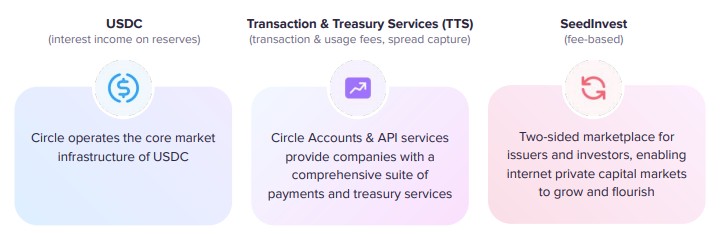

As previously mentioned, Circle operates through three primary business segments. The company outlines these in its investor presentation as follows:

Let's examine each of these areas, beginning with USDC.

Let's examine each of these areas, beginning with USDC.In recent times, stablecoins have gained considerable traction. These digital currencies, pegged to a stable external value, function as a unique form of cash within the cryptocurrency ecosystem. They provide a means of having on-chain purchasing power without the volatility and potential tax implications associated with other cryptocurrencies that might need to be sold to acquire assets. Stablecoins effectively merge the stability of currencies like the U.S. dollar with the innovative financial capabilities of the crypto space.

According to Circle, its USDC stablecoin is designed to be “compliant with both U.S. Federal and State regulations and guidelines for digital currency” and is built on leading blockchains such as Ethereum. What is the precise nature of Circle’s involvement with USDC? The company clarified this in a statement earlier this year:

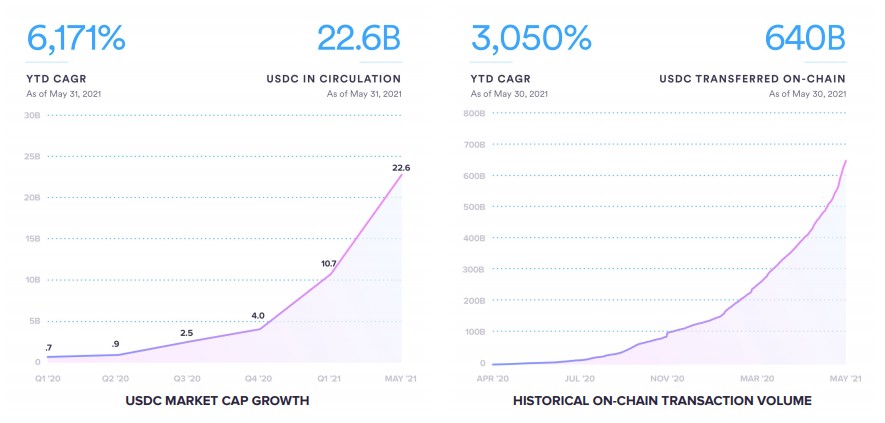

USDC has experienced substantial growth throughout its history. The following data, provided by the company, illustrates the usage of USDC since the beginning of 2020:

Analyzing these charts reveals a growing demand for stablecoins within the crypto market, with USDC capturing a significant portion of that demand. Data from CoinMarketCap confirms this trend; as of today, USDC’s market capitalization has reached $25.9 billion, positioning it as the second-largest stablecoin, trailing only Tether.

Analyzing these charts reveals a growing demand for stablecoins within the crypto market, with USDC capturing a significant portion of that demand. Data from CoinMarketCap confirms this trend; as of today, USDC’s market capitalization has reached $25.9 billion, positioning it as the second-largest stablecoin, trailing only Tether.USDC is not merely a secondary project for Circle; it is integral to the company’s core business model.

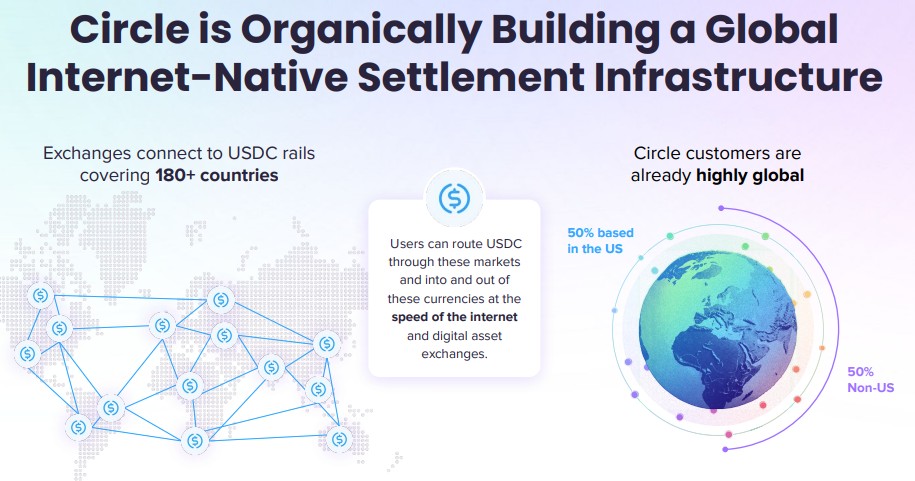

Consider the following slide:

USDC forms the foundation of Circle’s infrastructure, or, more precisely, Circle’s operations are built around USDC and its associated account system.

USDC forms the foundation of Circle’s infrastructure, or, more precisely, Circle’s operations are built around USDC and its associated account system.Further clarification is provided by this slide excerpt:

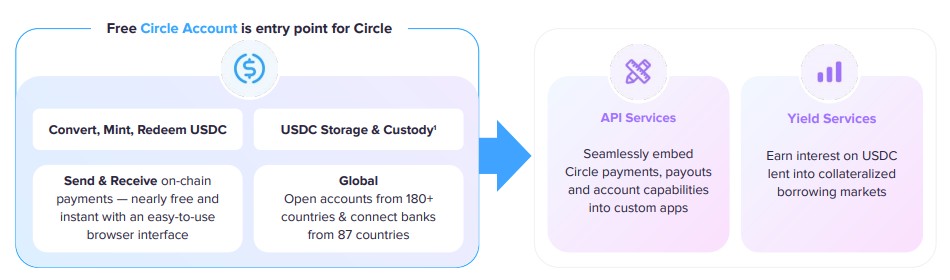

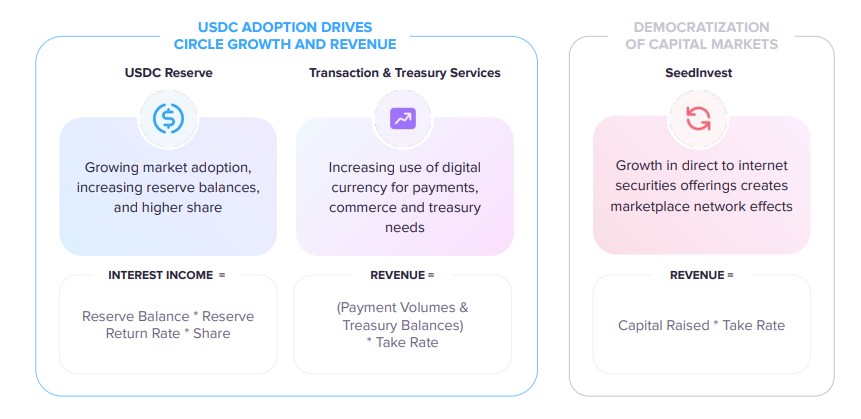

Circle accounts enable customers to interact with USDC and access the company’s API tools and yield-generating opportunities. Circle’s developer tools provide access to accounts, payments, payouts, and yield services. The company refers to these API services as “transaction and treasury services,” which aptly describes their function.

Circle accounts enable customers to interact with USDC and access the company’s API tools and yield-generating opportunities. Circle’s developer tools provide access to accounts, payments, payouts, and yield services. The company refers to these API services as “transaction and treasury services,” which aptly describes their function.Here’s a breakdown of how each of the company’s three business areas generates revenue:

Regarding revenue from reserves (located on the far left of the image), remember that stablecoins are pegged to a fiat currency and are backed by corresponding reserves. Therefore, when a large number of users purchase USDC from Circle, the company holds a substantial amount of cash reserves. Interest can be earned on these funds, and this revenue stream is likely to increase as interest rates rise. Consequently, a positive outlook on U.S. central bank tightening policies could translate to a positive outlook for Circle’s USDC reserve-related income.

Regarding revenue from reserves (located on the far left of the image), remember that stablecoins are pegged to a fiat currency and are backed by corresponding reserves. Therefore, when a large number of users purchase USDC from Circle, the company holds a substantial amount of cash reserves. Interest can be earned on these funds, and this revenue stream is likely to increase as interest rates rise. Consequently, a positive outlook on U.S. central bank tightening policies could translate to a positive outlook for Circle’s USDC reserve-related income.The central portion of the slide represents the culmination of the concepts discussed thus far. The company’s API-delivered services generate fee income based on usage volume. This model is well-understood within the technology sector, both within and outside of the cryptocurrency space.

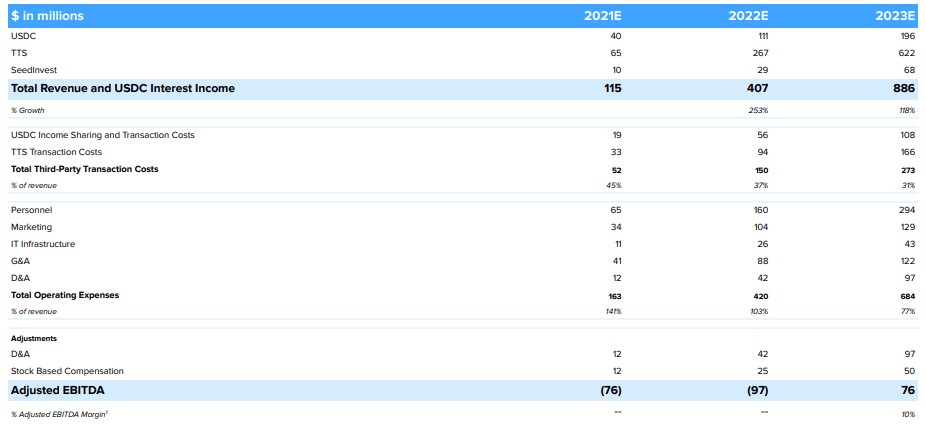

How do the three business segments compare in terms of revenue generation? Currently, this information is not available historically. However, Circle does provide projected results for its business units:

Beginning with the 2021 column, Circle projects USDC-related revenues of $40 million and API-delivered services revenue of $65 million. SeedInvest, which now appears to be a separate business following a review of the company’s presentation, is expected to generate less than 10% of the company’s total revenue for 2021.

Beginning with the 2021 column, Circle projects USDC-related revenues of $40 million and API-delivered services revenue of $65 million. SeedInvest, which now appears to be a separate business following a review of the company’s presentation, is expected to generate less than 10% of the company’s total revenue for 2021.Circle anticipates significant growth in both 2022 and 2023, forecasting a 253% increase in revenue in 2022 and a further 118% increase in the following year. This would scale the company from $115 million in revenue in 2021 to $886 million in 2023.

The second part of the table focuses on the cost of revenues. The company expects its “gross margins” to improve from 55% in 2021 to 69% in 2023. Achieving this would be a positive development.

The combination of anticipated revenue growth and improved margins is projected to lead to adjusted profitability in 2023, although the company would still report net losses due to higher operating expenses as a percentage of revenue than its gross margin.

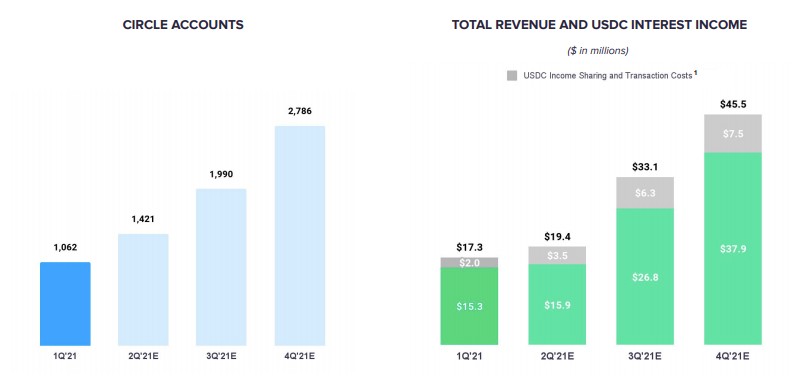

Historical data is limited to a single quarter. Here it is:

As of the end of March, the company had just over 1,000 Circle accounts – representing its customer base – and generated $17.3 million in first-quarter revenue. The company expects this figure to increase to $19.4 million in the second quarter.

As of the end of March, the company had just over 1,000 Circle accounts – representing its customer base – and generated $17.3 million in first-quarter revenue. The company expects this figure to increase to $19.4 million in the second quarter.It’s important to note that the company is separately reporting income-sharing and transaction costs related to USDC activity. This may indicate that these costs are deducted from revenue, and therefore, the company’s top-line projections may warrant further scrutiny. Nevertheless, the company is signaling to investors that its revenue growth is poised to accelerate in the third quarter.

We are examining a situation typical of a SPAC transaction. The company is merging and going public with limited historical financial data. Due to a history of business model adjustments, it doesn’t seem inclined to share extensive historical results. While this is legally permissible, it does raise some concerns.

This type of business is well-suited for a SPAC-led public offering. It would likely face challenges going public through a traditional initial public offering given its current stage of development. However, a SPAC can provide a substantial capital infusion at a predetermined price, allowing the company to mature while being publicly traded. This represents a risk, but also an opportunity to observe its progress.

The company anticipates the transaction will be completed in the fourth quarter of 2021, providing more data from Circle before it begins trading.

As of the last check, there were no new SEC filings from the SPAC entity containing more detailed, GAAP-compliant financial information. Therefore, we are currently relying on projections.

Regarding valuation, with an equity valuation of $5.4 billion, Circle is banking on rapid growth before the merger is finalized, effectively reducing its revenue multiple before trading begins.

Here’s the company’s revenue multiple based on its Q1 (actual) and Q4 (estimated) revenue, including revenue categorized as “income sharing and transaction costs:”

- Q1 revenue multiple: 78x

- Q4 revenue multiple: 29.7x

The difference is significant. Currently, Circle appears expensive relative to its scale. However, by the quarter the deal is expected to close, its valuation becomes more reasonable.

The market’s demand for shares in this company remains uncertain, but it has secured substantial capital to support its vision and model. We will gain further insights from its Q2 2021 and Q3 2021 results when they are released.

Related Posts

Coinbase Resumes Onboarding in India, Fiat On-Ramp Planned for 2024

David Sacks and Trump Administration: Potential Profits Examined

Benchmark Invests $17M in Crypto Trading App FOMO - Series A

Coinbase CEO Brian Armstrong on Prediction Markets - A Troll?

Anatoly Yakovenko on Agentic Coding | Solana News