Fintech Frugality: Lessons from Industry Leaders

Fintech Funding Surges to New Heights

Fintech companies supported by venture capital secured a record-breaking $30.8 billion in funding during the second quarter of the current year. This represents a substantial 30% increase when compared to the corresponding period last year.

The pace of investment is also accelerating, with companies receiving funding more quickly and in larger amounts. Currently, the average deal size is $47 million.

How is the Capital Being Utilized?

As a consequence of this influx of capital, fintech founders now have significant financial resources at their disposal. This raises the question of how these funds are being allocated.

Challenges in Tracking Spending Trends

Analyzing spending patterns proves difficult, as comprehensive data from both private and public companies doesn't reveal clear trends. However, insights into effective capital allocation may be readily available if examined closely.

Determining how efficiently capital is deployed remains a key area of investigation for industry observers.

Examining Top Performers in Fintech

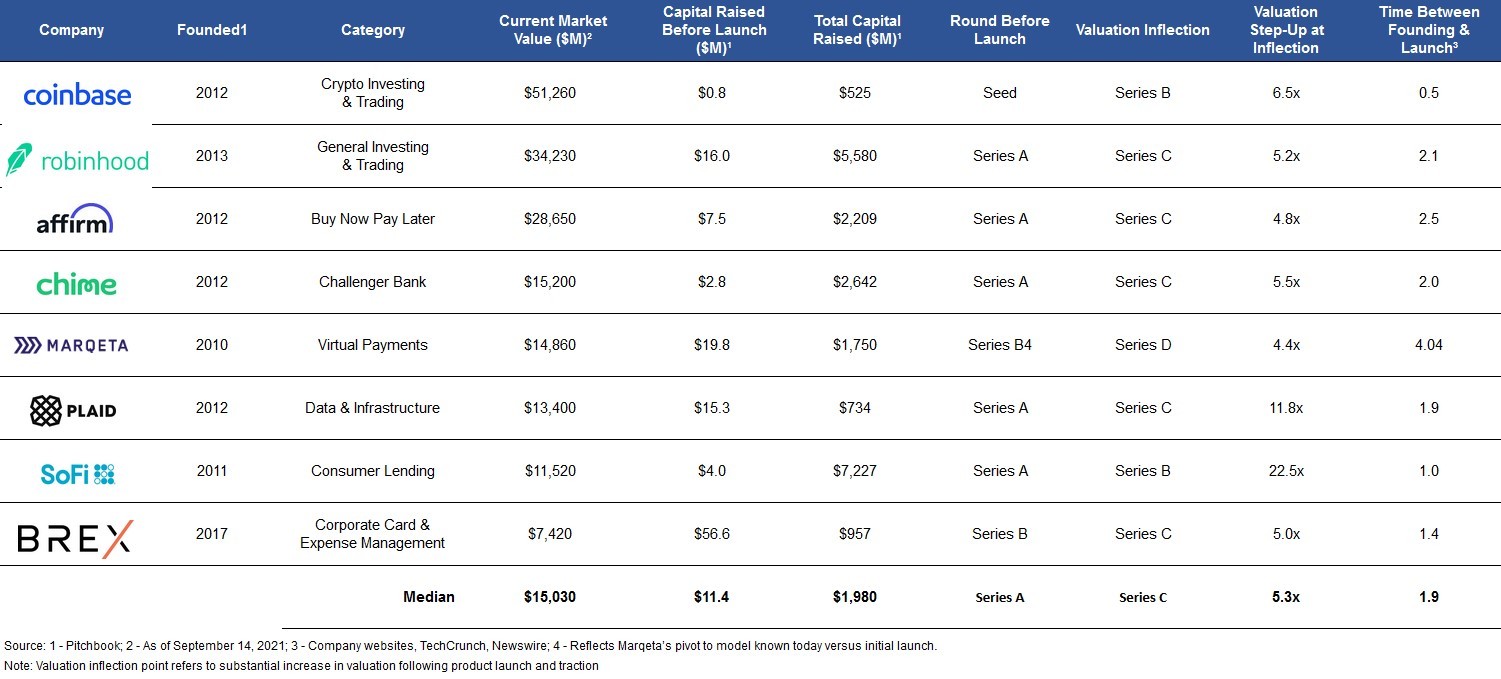

A growing number of fintech startups are now valued at $10 billion or more. The following list showcases some of the most notable examples. By analyzing their capital allocation strategies, we can gain valuable insights into how they achieved their current standing within the industry.

It’s true that variations in business models, differing target markets, and a decade-long fundraising period could complicate the extraction of meaningful conclusions. However, their patterns of fundraising and company development suggest otherwise.

Key Strategies for Success

Analyzing these fintech “leaders” reveals fundamental principles regarding how they secured funding and constructed their businesses. A significant number of these companies dedicated approximately two years to development before launching their product and then rapidly expanded with relatively modest capital investments, often even prior to a Series A funding round.

This approach contrasts sharply with the current fundraising landscape. These companies prioritized cultivating early adopters – both among customers and distribution partners – enabling growth and scalability without relying on enterprise sales.

Eventually, each of these businesses secured substantial funding rounds. These rounds represented an impressive 174x multiple of the capital initially raised before the product’s launch. However, they strategically delayed these large raises until after their product had already gained market acceptance.

These successful companies consistently demonstrate three shared characteristics.

These successful companies consistently demonstrate three shared characteristics.Common Traits of Leading Fintech Companies

- Focused Development: A period of dedicated product development precedes market launch.

- Early Adoption: Cultivating a base of initial customers and partners is crucial.

- Strategic Fundraising: Large funding rounds are pursued *after* product validation.

These principles highlight the importance of a measured and strategic approach to building a fintech business. Prioritizing product-market fit before aggressively seeking capital appears to be a common denominator among these industry frontrunners.

A Critical Valuation Stage

Despite variations in their business approaches, target markets, and founding dates, the analyzed companies consistently demonstrated a specific valuation inflection point. Typically, these organizations initiated product release following their Series A funding, then leveraged Series B capital to accelerate growth, ultimately experiencing a fivefold increase in valuation during the Series C round.

A significant number of these companies prioritized robust product development over a period of several years prior to launch. This allowed for rapid scaling immediately after release. For example, Plaid acquired over 10 million users within its first six months, and Brex onboarded more than 1,000 businesses in its initial year.

This considerable momentum served as a strong signal of product-market fit. They strategically utilized the funds from their Series A to refine their product, and subsequently expanded operations using the proceeds from Series B.

Capitalizing on Momentum

Substantial capital raising occurred after product launch and the identification of key early adopters, rather than before. This approach allowed these companies to effectively fuel viral growth.

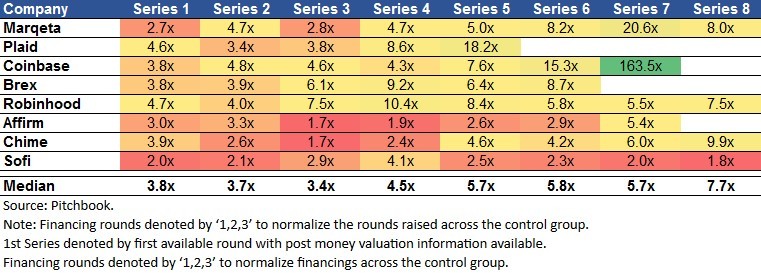

Even during subsequent funding rounds, these businesses demonstrated capital efficiency compared to their competitors. Analysis of data from up to eight rounds reveals that this group of leaders raised less capital in each round, and on average, relinquished 3% less equity across those eight funding stages.

Further data suggests this commitment to fiscal responsibility extended beyond the initial growth phases. Coinbase notably did not seek additional funding prior to its IPO, a noteworthy decision given the common practice of raising equity to satisfy public investor expectations at the time of public offering.

Further data suggests this commitment to fiscal responsibility extended beyond the initial growth phases. Coinbase notably did not seek additional funding prior to its IPO, a noteworthy decision given the common practice of raising equity to satisfy public investor expectations at the time of public offering.Similarly, Brex limited equity sales to under 6% following its Series C, contrasting sharply with the substantial capital infusions seen by competitors like Ramp.

Exceptions to the Rule

Companies offering credit or lending-based products, such as Sofi and Affirm, represented exceptions to this trend. Their business models necessitate a combination of debt and equity to fulfill balance sheet requirements inherent in lending operations, leading to greater capital needs.

- These companies required significant capital due to the nature of their lending products.

- Sofi and Affirm’s models depend on managing both debt and equity.

The Power of Resourcefulness in Business Growth

Each of these eight companies demonstrated remarkable resourcefulness during their formative years, a characteristic even more pronounced when viewed through today’s investment landscape. Marqeta, for instance, flourished under conditions of financial constraint, implementing a weekly budgeting system prior to its 2015 strategic shift. This approach coincided with a period of consistent revenue doubling, ultimately culminating in a successful IPO.

Despite undergoing three distinct business model iterations, the company consistently prioritized efficiency. This ultimately led to the development of the innovative issuer-acquirer model that defines its current operations.

Limited Funding, Focused Development

A key observation is the relatively modest funding rounds secured by these platforms during their initial product development phases. There was considerable skepticism surrounding Brex’s ambition to challenge established banking institutions, as such a feat seemed improbable at the time. Similarly, the potential for a cryptocurrency exchange to achieve a $100 billion valuation was widely doubted.

Access to consumer account data, a cornerstone of Plaid’s business, was also considered unlikely to be granted freely by traditional banks. Consequently, securing funding exceeding $100 million proved challenging for these ventures. Interestingly, increased capital investment did not consistently translate into greater revenue or more substantial competitive advantages.

Beyond First-Mover Advantage

Notably, the majority of these platforms were not pioneers in their respective fields. Their current market dominance is particularly striking given the need to overcome the advantages held by earlier entrants with greater resources. Simple, established in 2009, enjoyed a three-year lead over Chime and benefited from BBVA’s financial backing after raising nearly $16 million, yet ultimately failed to achieve Chime’s scale and was discontinued.

Finicity had already secured $80 million in funding by the time Plaid was founded in 2012, as reported by PitchBook. Robinhood also entered a market already populated by competitors like eToro.

Frugality as a Catalyst for Innovation

The substantial head starts and significant capital reserves enjoyed by first movers did not guarantee success. While some companies, such as Marqeta and Affirm, successfully established themselves as category leaders, the varied outcomes within this fintech cohort underscore a crucial point.

Capital raised and early market entry are not definitive predictors of market leadership. The pressures of operating with limited resources can, in fact, foster the innovation necessary to surpass competitors and achieve lasting success.

The Importance of Early Champions in Fintech Growth

Many successful fintech companies achieved significant growth by identifying and cultivating key champions early in their development. A prime illustration of this is Marqeta's relationship with Square, which currently generates $357 million in annual revenue and continues to expand.

Comparable instances of success were observed across various business models. Affirm's collaboration with Shopify, initiated just one year after its launch in 2015, dramatically accelerated its expansion among merchants.

Brex benefited from a champion within Y Combinator, granting access to and establishing credibility with numerous startups, which subsequently drove its widespread adoption. Stanford University, the founder’s former university, provided SoFi with a crucial beta testing opportunity.

This initial support led to the formation of over a hundred university partnerships within a few years of the company’s inception.

Cultivating these early champions – whether customers or distribution partners – proved essential for the rapid adoption and scaling of these fintech leaders.

Leveraging this organic growth, tied to increasing payment and transaction volumes, has allowed certain segments of the fintech sector to achieve forward multiples exceeding 20x in public markets.

Key Strategies for Champion-Based Growth

- Identify Potential Champions: Focus on early adopters who recognize the value proposition.

- Nurture Relationships: Provide exceptional support and actively solicit feedback.

- Scale with Growth: Align your infrastructure to accommodate increasing transaction volumes.

- Leverage Credibility: Utilize champion endorsements to build trust with a wider audience.

The ability to grow alongside a champion is a powerful driver of success in the competitive fintech landscape.

Demonstrating Financial Success

Ultimately, concrete financial results are the most persuasive evidence. A key takeaway from this analysis is the substantial return on investment realized by leading companies in the fintech sector, across various funding stages.

Following initial funding rounds, these fintech companies consistently demonstrated a median return on invested capital exceeding 3.4x. This figure rose to over 7.5x with the successful exits and later funding rounds of companies like Marqeta, Robinhood, Chime, and Sofi. These numbers are remarkably high when contrasted with the S&P 500’s average 10-year return of 14%.

Understandably, the complete dataset includes some exceptional cases. The opportune timing of Coinbase’s IPO and the resulting 163.5x return on invested capital at exit are unique. Similarly, Sofi’s comparatively lower return reflects its more capital-intensive operational model.

However, assuming rational public and private markets, the consistent strength of return on investment throughout these companies’ growth suggests efficient capital allocation. This indicates a strategic approach to resource deployment at each stage of development.

While this return on investment isn't a direct measure of core business strengths like recurring revenue or unit economics, the consistency and scale of these returns present a strong case. Frugality appears to be deeply ingrained in the culture of these successful companies, as integral as the technology fueling their growth.

Key Insights

Key InsightsWhile these past observations might seem limited to their time, their significance persists, especially within the rapidly evolving landscape of today’s innovation-driven economy. The central point remains valid, and is arguably even more crucial now, as both investors and entrepreneurs strive for substantial results to justify escalating funding rounds and valuations: Capital can stimulate expansion, but it cannot ensure a fundamentally sound enterprise.

It is evident that a groundbreaking concept, a determined leadership team, and a product designed to deliver exceptional value to the end-user are the foundational elements of achievement. This essential synergy is not something that can be acquired through publicity or a substantial investment of $100 million.

A truly successful venture requires more than just financial backing.

Essential Components for Success

- A disruptive idea that challenges the status quo.

- An unyielding founder with unwavering commitment.

- A product meticulously crafted to provide a superior customer experience.

These three elements, working in concert, represent the true drivers of lasting success.

Note: The perspectives expressed here are solely those of the author and do not necessarily align with the views of SVB Capital.

Related Posts

21-Year-Old Dropouts Raise $2M for Givefront, a Nonprofit Fintech

Monzo CEO Anil Pushed Out by Board Over IPO Timing

Mesa Shutters Mortgage-Rewarding Credit Card

Coinbase Resumes Onboarding in India, Fiat On-Ramp Planned for 2024

PhonePe Pincode App Shut Down: Walmart's E-commerce Strategy