SoftBank Vision Fund's Summer Turnaround: From Losses to Profits

Considering the unusual circumstances of 2020, it can be challenging to recall the period dominated by the Vision Fund. However, SoftBank’s highly ambitious investment fund ceased making new investments just last September, concluding its allocation of substantial capital from a total commitment of approximately $99 billion.

The Vision Fund operated with significant influence, readily investing large sums into selected companies and prioritizing accelerated expansion. Calculations by TechCrunch indicate that, throughout its investment period, the first Vision Fund invested roughly $100 million each day.

The Exchange provides analysis of startups, markets, and financial matters. It is published daily on Extra Crunch, and a newsletter version is available every Saturday.

Even prior to SoftBank and its founder, Masayoshi Son, completing their investment activities, challenges began to emerge. In 2019, TechCrunch documented a series of difficulties within the portfolio, including workforce reductions at Wag, a disappointing initial public offering for Uber, difficulties at Brandless, the failed WeWork IPO and the subsequent problems, leadership transitions at Compass, layoffs at Fair and Katerra, and a weak public debut for OneConnect.

The year 2020 continued these trends, with further issues at OYO, job cuts at Zume Pizza, and criticism for breaches of agreed-upon investment terms.

By April of this year, SoftBank acknowledged that its Vision Fund investments were likely to result in considerable losses, contributing to an unusual annual loss for the company when combined with other investment setbacks.

Subsequently, the situation improved: SoftBank’s Vision Fund experienced a notably stronger performance in the latter half of the year than many anticipated, and it’s important to understand the reasons behind this turnaround.

Therefore, we will examine the relevant data, acknowledge the consistent presentation style employed by SoftBank in its reports, and explore the factors that led to the Vision Fund’s improved results.

A Resurgence

Prior to examining the recent improvements, it’s essential to first consider the financial challenges the Vision Fund presented to its parent company earlier in the year.

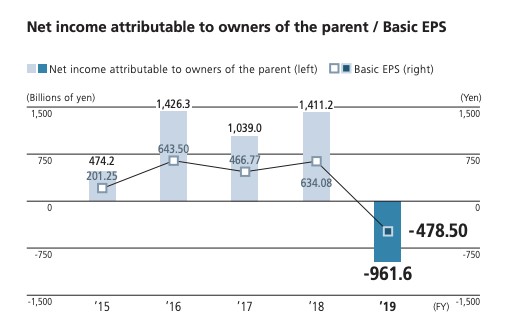

To fully understand the impact of the Vision Fund’s difficulties on SoftBank Group during the 12-month period concluding on March 31, 2020, a single graphic provides all the necessary insight. Here’s a depiction of SoftBank Group’s net income throughout its fiscal year 2019:

The reported loss for this period is particularly noticeable.

The reported loss for this period is particularly noticeable.What was the primary cause of this deficit? A ¥1.9 trillion loss attributed to the Vision Fund, resulting from declines in the “fair values of Uber and WeWork and its three affiliates,” as well as a significant decrease in the fair value of “other portfolio companies” during the fourth quarter, largely due to the effects of the COVID-19 outbreak.

It proved to be a difficult and humbling experience to commit substantial capital with such optimism, only to see so many investments perform poorly.

At the close of fiscal year 2019, SoftBank Group stated that the Vision Fund held 88 investments totaling $75 billion in cost. The entire group’s value was $69.6 billion, “excluding exited investments.”

Looking ahead to the company’s most recent report, covering the subsequent six months – a period ending with the close of September – a comparison of the two sets of results is striking: SoftBank Group had returned to profitability, demonstrating strong year-over-year gains compared to the same period in the previous fiscal year.

It’s important to note that SoftBank Group encompasses more than just the Vision Fund; it is a major Japanese conglomerate with a substantial and profitable telecommunications business. However, our focus is on its startup investment performance, so how did the Vision Fund itself contribute to the company’s results in the six months ending September 2020?

- Vision Fund 1 generated realized gains of ¥141.4 billion through the sale of “a portion of its shares in four portfolio companies.”

- Vision Fund 1 reported unrealized gains of ¥804.8 billion, driven by “¥374.5 billion gain on investments in listed portfolio companies due to a recovery in the public equity markets, and ¥430.3 billion on investments in unlisted portfolio companies,” a subject we will revisit.

- Vision Fund 2 reported unrealized gains of ¥537.2 billion, primarily stemming from strong post-IPO gains in the value of KE Holdings.

The fact that the first Vision Fund realized profits from selling shares in some of its companies was not unexpected. Similarly, the positive performance of the second Vision Fund on an investment that went public and increased in value, while positive, isn’t the central point of our analysis.

Instead, we must determine what factors changed within the Vision Fund 1 portfolio between March and September that dramatically altered the trajectory – and therefore the value – of the companies it included.

SoftBank explains this through its discussion of Vision Fund 1’s unrealized gains, stating they were “driven by the fair value uplift of portfolio companies where exits have been decided or have new funding rounds, or have benefited from the accelerated adoption of digital services following the COVID-19 pandemic.”

This observation is both insightful and unsurprising. It’s insightful because the same forces that broadly benefited startups – the accelerating shift to digital transformation in response to widespread remote work, the surge in e-commerce due to the pandemic, and so on – also positively impacted the Vision Fund’s performance. It’s unsurprising because it doesn’t represent a complex strategy or unexpected event; we’ve come to anticipate the unexpected from the Vision Fund, not the benefit of widespread market trends.

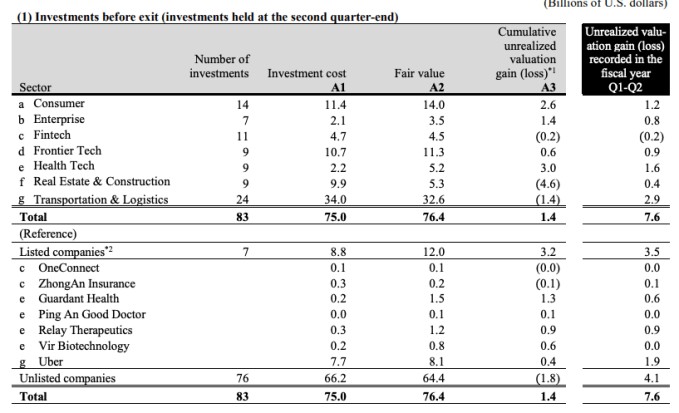

According to SoftBank, Vision Fund 1 concluded the first half of its fiscal year 2020 with 83 investments costing $75 billion, now valued at $76.4 billion, a significant improvement from the previous report which showed SoftBank operating at a loss when comparing investment cost to current value.

Where did these gains originate? The following table details all investments within Vision Fund 1, their initial cost, and their current fair value, expressed in billions of dollars:

Of the $7.6 billion in gains realized during the first two quarters of fiscal year 2020, $4.1 billion came from its privately held investments and $3.5 billion from its public investments, with Uber accounting for slightly more than half of the latter.

Of the $7.6 billion in gains realized during the first two quarters of fiscal year 2020, $4.1 billion came from its privately held investments and $3.5 billion from its public investments, with Uber accounting for slightly more than half of the latter.Among the private companies in the Vision Fund 1 portfolio, those in the transportation and logistics sectors performed the best – unsurprisingly, given the e-commerce boom – followed by companies categorized as “health tech” and then “consumer.”

Notably, the only sector of private investments within the Vision Fund 1 portfolio to experience a decrease in value was its collective fintech investments. It is interesting to consider what percentage of venture-style investors experienced losses on fintech deals in 2020? It is likely a small number.

Regardless, after enduring setbacks throughout calendar year 2019 and the first couple of months of calendar year 2020, SoftBank Group has returned to profitability, partially due to gains within its Vision Fund 1 portfolio. This is a positive development, as the company is currently making new investments from its second fund using its own capital.

As promised, a few humorous observations!

Presented here, from the SoftBank Group presentation, is a depiction of all of human history in a single slide:

Presented here, from the SoftBank Group presentation, is a depiction of all of human history in a single slide:The reference to AI is intentional. Here’s SoftBank’s perspective on which companies are poised for success in the coming years:

And which companies are currently leading the way in this arena?

And which companies are currently leading the way in this arena? Indeed.

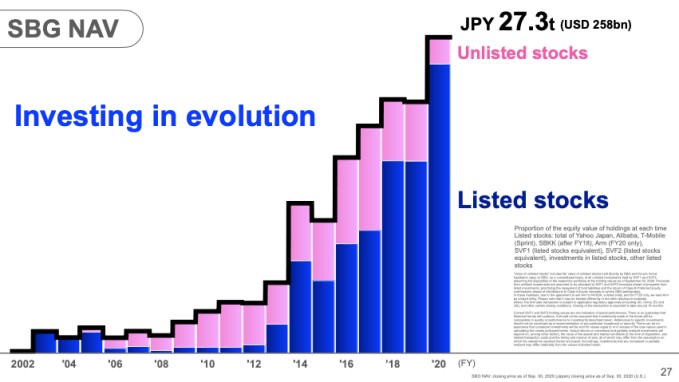

Indeed.In any case, let’s examine what that future might entail! Here’s a breakdown of SoftBank’s investment history to date, categorized by private and public investments:

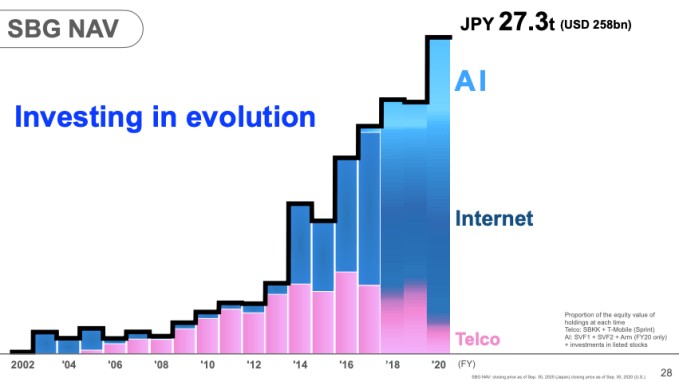

And here’s the same data, segmented by investment theme:

And here’s the same data, segmented by investment theme: A decline in telecom investments, substantial internet investments, and a growing proportion of AI-focused deals. Given that AI is anticipated to shape the future, this chart is not surprising, aside from its color scheme.

A decline in telecom investments, substantial internet investments, and a growing proportion of AI-focused deals. Given that AI is anticipated to shape the future, this chart is not surprising, aside from its color scheme.But based on this foundation, where will SoftBank’s investments go next? This was the question the company sought to answer:

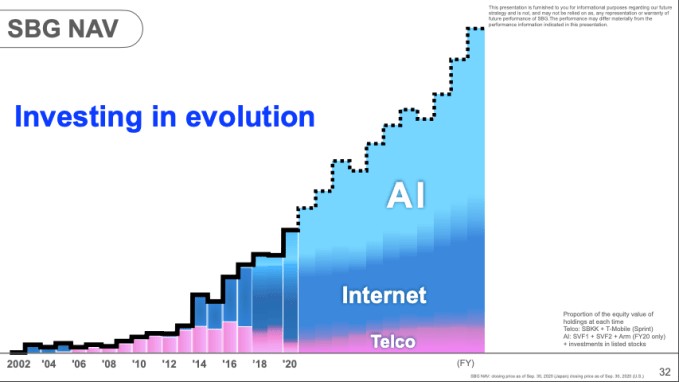

Here’s their own projection:

Here’s their own projection: Apparently, increased investment in AI will enable SoftBank Group to surpass Berkshire Hathaway. This outcome may be realized if Uber’s stock continues to appreciate.

Apparently, increased investment in AI will enable SoftBank Group to surpass Berkshire Hathaway. This outcome may be realized if Uber’s stock continues to appreciate.Regardless, you are now fully informed about Vision Fund 1 and its recovery. Now, back to your work!

Related Posts

Trump Media to Merge with Fusion Power Company TAE Technologies

Radiant Nuclear Secures $300M Funding for 1MW Reactor

Coursera and Udemy Merger: $2.5B Deal Announced

X Updates Terms, Countersues Over 'Twitter' Trademark

Slate EV Truck Reservations Top 150,000 Amidst Declining Interest