Huawei IoT Growth: Diversifying Beyond Smartphones

Huawei Diversifies Beyond Smartphones Amid Trade Challenges

Facing difficulties stemming from U.S.-China trade disputes, Huawei is actively exploring opportunities in a wider range of smart devices. This strategic shift positions the company in direct competition with numerous hardware manufacturers both domestically and internationally.

Financial Performance in 2020

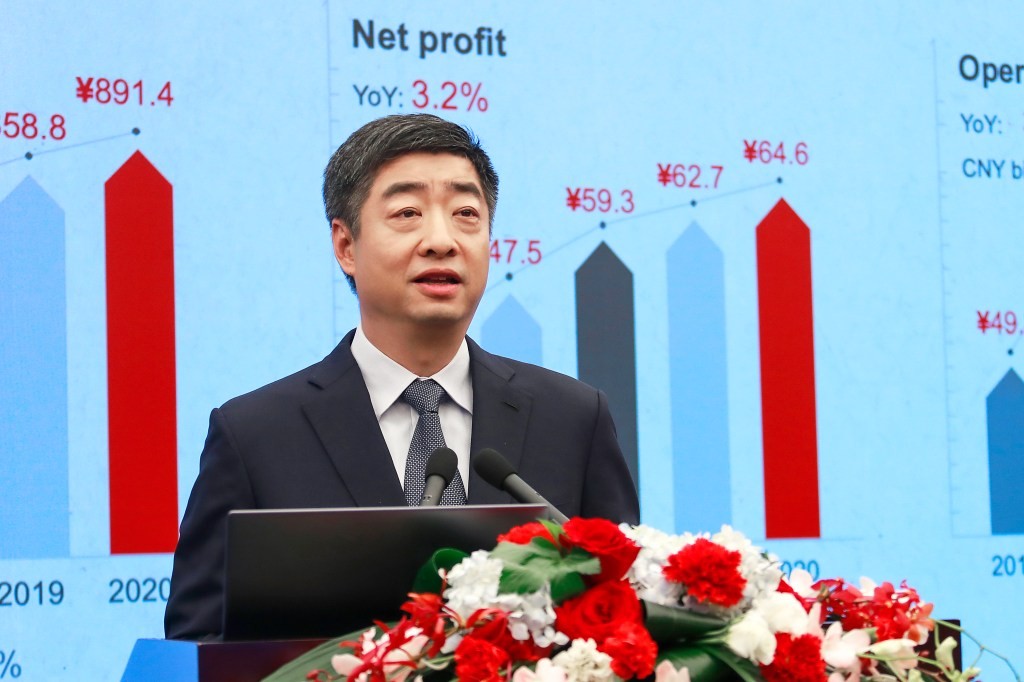

Huawei experienced comparatively modest revenue growth in 2020, increasing by only 3.8% to 891.4 billion yuan ($136 billion). Net profit also saw a smaller rise, reaching 64.6 billion yuan, a 3.2% increase. These results aligned with the company’s prior projections, as revealed during its annual report presentation in Shenzhen.

For context, Huawei’s revenue growth in 2019 and 2018 was significantly higher, at 19% and 19.5% respectively.

Impact of U.S. Export Controls

The deceleration in 2020 was largely attributable to a decline in Huawei’s international smartphone sales. U.S. export restrictions limited the company’s access to essential chipsets and Google services, which are crucial for consumer appeal. However, these challenges have simultaneously accelerated Huawei’s efforts to diversify its product portfolio and mitigate losses within its mobile phone division.

Expansion into New Device Categories

Over the past two years, Huawei has significantly increased its investment in a diverse array of smart devices. These include AR/VR headsets, tablets, laptops, televisions, smartwatches, speakers, headphones, and in-car systems.

Huawei’s involvement in the automotive sector has garnered considerable attention, coinciding with the rapid expansion of the global smart vehicle industry. Recent reports suggested Huawei was planning to manufacture vehicles under its own brand, a claim the company has refuted.

Focus on Automotive Components and Services

At a recent event, rotating chairman Ken Hu emphasized that Huawei will concentrate on its core competencies. The company intends to supply specific automotive components and services, such as in-car operating systems and intelligent cockpit technologies, rather than producing complete vehicles.

Strategic Similarities and Differences

Huawei’s interconnected product ecosystem bears resemblance to Xiaomi’s IoT strategy, which is centered around its smartphones and operating system. A key distinction, however, is that Huawei also operates as a major provider of telecommunications infrastructure.

Resilience in the Carrier Segment

Despite exclusion from 5G rollout plans in some nations, including the United Kingdom, Huawei’s carrier segment maintained revenue levels comparable to the previous year. The COVID-19 pandemic proved beneficial, driving increased global demand for network solutions as remote work and learning became widespread.

Early Successes in IoT

Huawei’s IoT initiatives have demonstrated initial success, although the competitive landscape is intense. The company highlighted smartwatches as a significant contributor to its revenue growth in the past year.

Wearables Market Share

According to research from IDC, Apple maintained its leading position in the wearables market in 2020, capturing 34.1% of the market share. Huawei secured the third position with 9.8%, following its domestic competitor Xiaomi, which held 11.4% of total shipments.

Reliance on the Chinese Market

In 2020, Huawei’s growth was heavily reliant on its home market, with China accounting for 65.5% of its total revenue, a 15.4% year-over-year increase. Conversely, the company experienced revenue declines in other regions: a 12.2% decrease in Europe, the Middle East, and Africa; an 8.7% decline in the rest of Asia; and a substantial 24.5% drop in the Americas.

Related Posts

Pickle Robot Appoints Tesla Veteran as First CFO

Meta Pauses Horizon OS Sharing with Third-Party Headsets

Amazon Reportedly in Talks for $10B OpenAI Investment

Meta AI Glasses Enhance Hearing - New Feature

Whole Foods to Implement Smart Waste Bins from Mill | 2027