Udemy Files to Go Public: B2B Growth Fuels IPO

Udemy IPO Analysis: Following Duolingo's Footsteps

Following a detailed review of the Rent the Runway IPO documentation, our focus now shifts to Udemy's public offering.

The launch of Udemy’s IPO occurs after the successful initial public offering of Duolingo earlier in the year. This debut could be the last significant edtech IPO before Byju’s anticipated entry into the public market.

Market Implications and Investor Stakes

Udemy’s performance in its IPO is poised to influence other companies within the edtech sector, particularly those with substantial financial backing.

The Exchange provides insights into startups, markets, and financial matters.

Access it daily on Extra Crunch or subscribe to The Exchange newsletter on Saturdays.

A key question is how the company’s growth trajectory looks now that the surge in demand for edtech, fueled by the pandemic, has subsided.

Funding and Valuation

Udemy, an online learning platform, secured over $300 million in funding during its private phase.

A $50 million Series F round completed in late 2020 established the company’s valuation at just over $3.2 billion, according to Crunchbase data.

This IPO represents a significant opportunity for liquidity for investors including Lightbank, Insight Partners, Norwest Venture Partners, Mindrock Capital, and Tencent.

A Dual Business Model

Udemy operates with a distinctive two-pronged business structure, catering to both individual consumers and corporate clients.

To accurately assess Udemy’s financial health, a thorough examination of both segments of its business model is essential.

Understanding the shifts in the company’s overall revenue composition and its recent trends is also crucial.

This analysis promises to be insightful, and we are eager to delve deeper into the details.

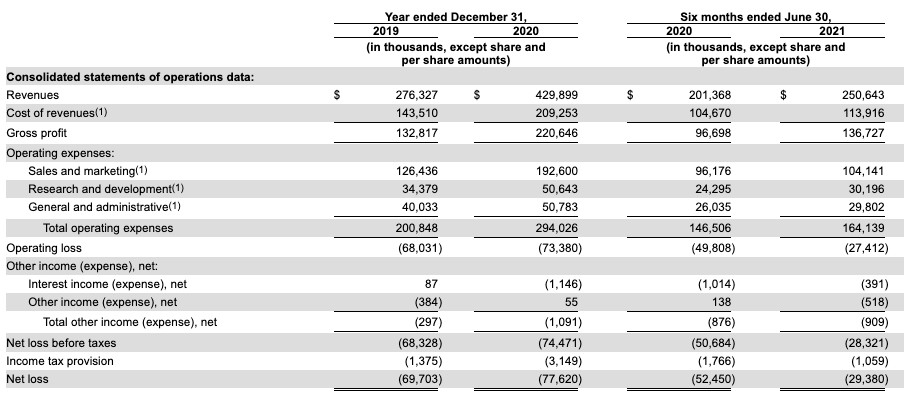

Udemy’s Performance During and After the Pandemic

Udemy experienced significant growth between 2019 and 2020, with revenue increasing from $276.3 million to $429.9 million. This represents a substantial rise of 55.6%. Such growth is particularly noteworthy for a company that had already achieved a considerable scale, exceeding $100 million in revenue.

In the first half of 2021, Udemy reported total revenues of $250.6 million. This figure demonstrates a 24.5% increase when compared to the first half of 2020.

However, a deceleration in growth was anticipated following the initial surge experienced during the pandemic. Therefore, the observed decline in revenue growth into 2021 is not entirely unexpected.

The manner in which investors will assess a larger, more profitable, yet slower-growing edtech company like Udemy will be a key factor to observe.

Currently, Udemy does not operate at a net profit. However, the company is demonstrably reducing its financial losses over time.

Adjusting for share-based compensation costs, Udemy’s net loss for H1 2020 can be reduced by $20.6 million, and the H1 2021 figure by $16.5 million.

Adjusting for share-based compensation costs, Udemy’s net loss for H1 2020 can be reduced by $20.6 million, and the H1 2021 figure by $16.5 million.This adjustment brings Udemy’s losses for the first half of 2021 down to under $13 million. This is a significant improvement compared to previous periods.

The company benefited from operating leverage during the pandemic, successfully reducing losses while simultaneously expanding its revenue base.

Revenue Composition

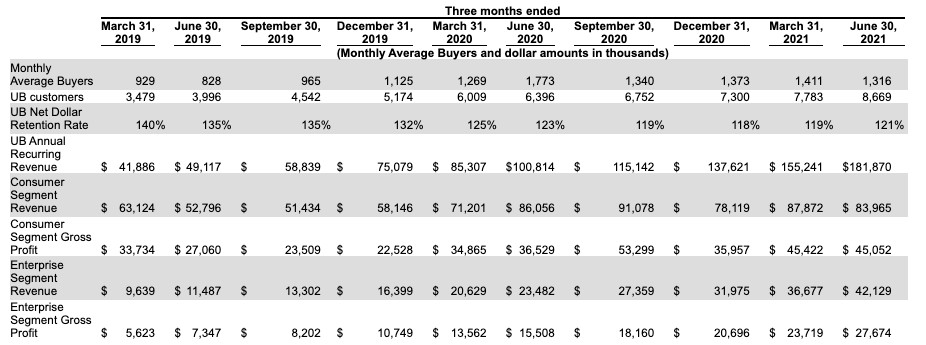

An exception will be made to our standard practice of excluding marketing-oriented charts from our S-1 analyses. This is due to the compelling data presented regarding Udemy’s revenue streams.

The provided chart effectively illustrates the shifting dynamics within the company’s revenue mix. A clear transformation is visible when comparing the data from Q4 2020 to Q2 2021.

According to the company’s documentation, the following key points highlight the changes in revenue composition:

Udemy experienced a decrease in consumer revenue contribution, moving from 82% in 2019 to 69% in the first half of 2021. This shift appears to be both significant and consistently progressing. Essentially, Udemy is transitioning from a consumer-centric model to one primarily focused on business customers, as reflected in revenue generation.

This development is likely a positive indicator for the edtech company. The reasoning is that “[s]ubstantially all of our consumer revenue is generated from individual course enrollments by consumers on our online platform,” Udemy states. This suggests a pattern of one-time purchases rather than sustained, recurring revenue streams.

Conversely, Udemy’s revenue from corporate clients is characterized by “[t]he majority of our customers subscribing to our [Udemy Business] offering through annual contracts, with an increasing trend towards multiyear agreements. Fees are largely determined by the number of user licenses.” This represents a B2B SaaS model, which is highly favored by investors.

Therefore, Udemy is evolving from a consumer-driven service with limited recurring revenue to a B2B SaaS enterprise. The growth in this latter revenue category has been substantial: 18% of Udemy’s 2019 revenue originated from its business segment, amounting to $52.5 million, compared to 31%, or $77.7 million, in the first half of 2021. To put it simply, Udemy’s business revenue in the first six months of 2021 was almost 50% higher than its total business revenue for the entire year of 2019.

Udemy anticipated investor interest in its business operations and provided detailed financial data for further analysis. The net dollar retention rate for Udemy Business revenue—demonstrating a focus on SaaS metrics—reached 121% in Q2 2021, the highest figure since Q2 2020. Furthermore, Udemy reported its business-focused annual recurring revenue at $181.9 million in the second quarter of 2021.

Examining the consumer revenue trend reveals the company’s pandemic-related surge, particularly from Q4 2019 through Q3 2020. These revenues subsequently decreased, while business recurring revenues continued to climb. Considering these figures, Udemy can be viewed as a B2B SaaS business with a pre-existing consumer business, potentially influencing valuation strategies.

Examining the consumer revenue trend reveals the company’s pandemic-related surge, particularly from Q4 2019 through Q3 2020. These revenues subsequently decreased, while business recurring revenues continued to climb. Considering these figures, Udemy can be viewed as a B2B SaaS business with a pre-existing consumer business, potentially influencing valuation strategies.Examining Profitability

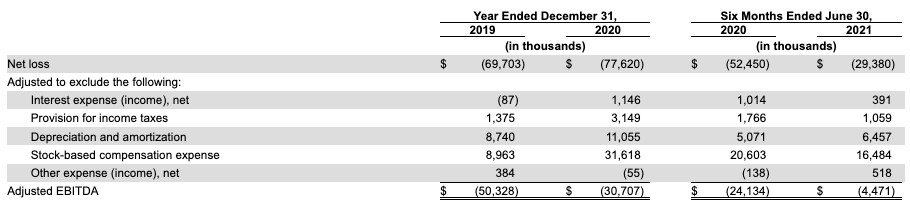

Our previous conversation briefly addressed net losses in relation to the company’s growth trajectory. Now, a detailed examination of adjusted profitability is warranted, as it is anticipated that investors in the public market will closely scrutinize these financial metrics.

The presented data indicates a positive trend, with Udemy approaching adjusted EBITDA breakeven during the first half of 2021. This progress should instill confidence in investors, suggesting that the period of adjusted losses may be nearing its conclusion. A combination of profit and growth is generally well-received.

The presented data indicates a positive trend, with Udemy approaching adjusted EBITDA breakeven during the first half of 2021. This progress should instill confidence in investors, suggesting that the period of adjusted losses may be nearing its conclusion. A combination of profit and growth is generally well-received.Valuation Considerations

Udemy presents a relatively stable consumer edtech component, integrated with a recurring-revenue B2B offering. Valuing Udemy solely on its business revenues, using its last private-market valuation, results in a multiple of 4.5x its Q2 2021 ARR. This valuation is remarkably low.

Furthermore, the consumer side of the business also contributes significant value. Therefore, it is reasonable to anticipate that Udemy will be priced at a level exceeding its final private-market valuation.

The specific pricing point remains to be determined. Further details will be provided once an initial pricing range is announced.

- Adjusted EBITDA: Udemy’s progress towards breakeven is a key indicator.

- B2B Valuation: The business revenue alone suggests an undervalued company.

- Consumer Business Value: The consumer side adds further to the overall worth.

Investors will likely focus on adjusted profitability as a crucial factor in their assessment. The company’s ability to demonstrate sustainable profits alongside continued growth will be paramount.

Related Posts

Peripheral Labs: Self-Driving Car Sensors Enhance Sports Fan Experience

Radiant Nuclear Secures $300M Funding for 1MW Reactor

Last Energy Raises $100M for Steel-Encased Micro Reactor

First Voyage Raises $2.5M for AI Habit Companion

on me Raises $6M to Disrupt Gift Card Industry